What are Research and Development Allowances

The forgotten or unknown capital allowance could be the most generous one available to you

The Government offers generous tax incentives for companies conducting R&D. Much media focus is on R&D tax relief schemes, which incentivise operational costs such as labour and materials; less attention is paid to maximising relief for capital costs linked to R&D.

However, for a lot of companies, capital allowances are the single most significant adjustment available to reduce taxable profits (typically only R&D tax relief rivals it for quantum); however, as capital allowances and R&D tax relief are often separately considered, many R&D companies are not fully maximising the capital allowances available to them.

Research and Development capital Allowances (RDAs) are less well-known than other capital allowances, such as Plant and Machinery Allowances (PMAs) and the Annual Investment Allowance (AIA).

100% Deduction

They offer a 100% deduction for any capital expenditure on R&D, which is as generous as capital allowances get.

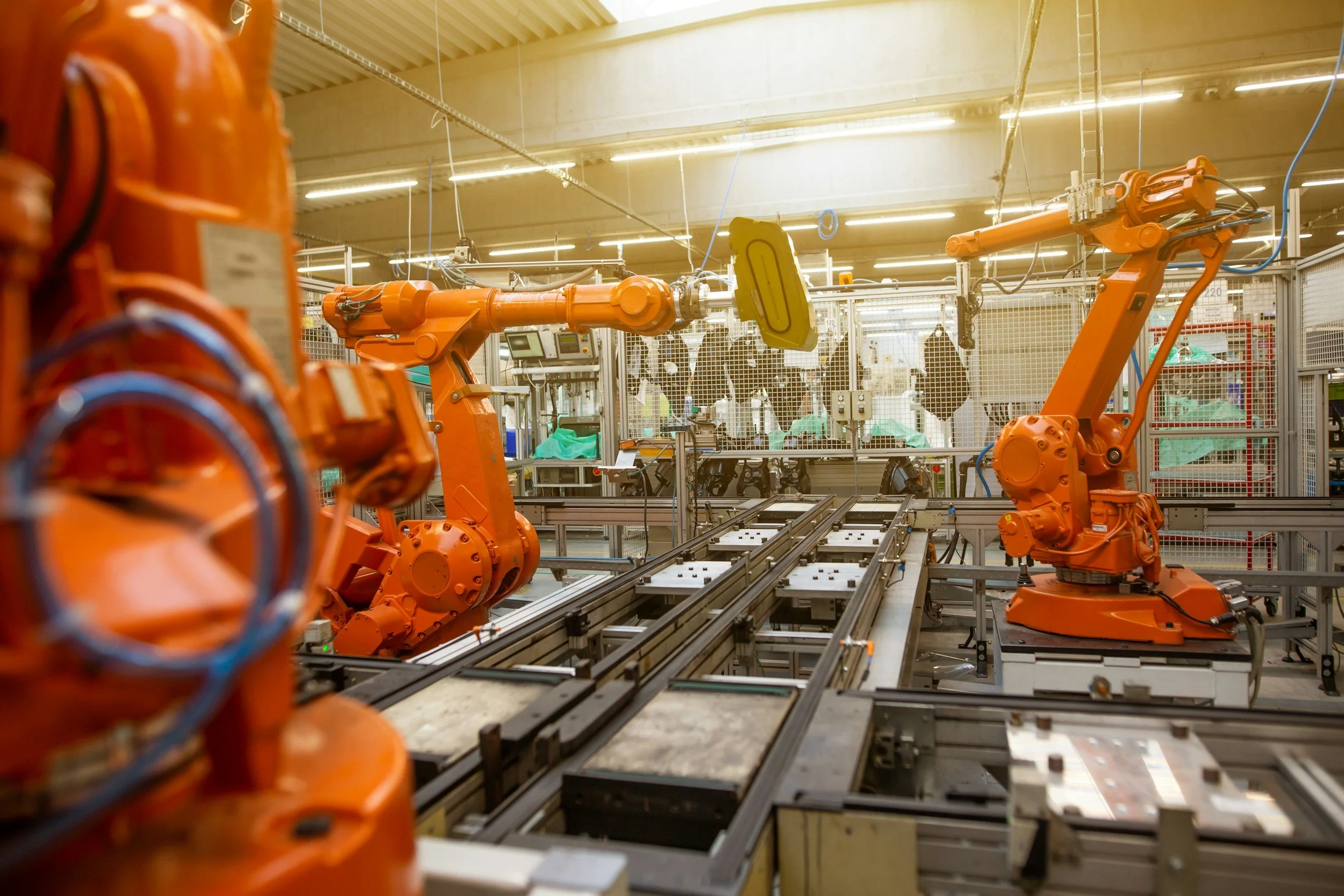

Capital Equipment

Expenditure eligible for RDAs includes the cost of purchasing capital equipment for use in R&D activities, and building, extending, refurbishing and sometimes purchasing property in which R&D activities take place.

No Limit

There is no limit on RDAs, so for companies spending more than £200k, RDAs can potentially sweep up the balance to maximise the deduction.

It is not possible to consider RDAs in isolation; this is because to optimise your relief for capital costs you need to understand the different types of capital allowances and how they interact. Each case needs to be considered on its own facts and circumstances. For example, the AIA was introduced in 2008 to simplify the calculation of capital allowances for smaller businesses by allowing all plant and machinery costs, up to a set maximum, to be deducted in full for tax purposes. Since its introduction, it has been the subject of much tinkering – rising from an initial level of £25k per annum right up to £500k, and recently down again to £200k and then back up to £1,000,000 until December 2021.

Effectively, the AIA and RDAs are both types of capital allowance which offer a 100% deduction for certain capital expenditure;expenditure may fall into both but can only be claimed under one.

So…if they both offer the same rate of relief, why worry about RDAs?

1 – They are not always the same type of expenditure.

For AIA, that capital expenditure must be incurred on plant or machinery, i.e. costs that would otherwise fall under the far less generous PMAs. RDAs, however, may be claimed for any capital expenditure on R&D, excluding land costs. Whilst this may include the same plant and machinery that you can use the AIA for, it also includes build costs, which do not generally attract any other form of tax deduction.

2 – If you are spending more than £200k per annum.

From 1 January 2016, the AIA will be £200k per annum, rising to £1 million from 2020 onward, so whilst the RDA will have less impact for companies in the future, there is still an opportunity to claim the benefit an RDA would give if you are at the moment.

Without RDA’s, these costs would fall into PMAs, attracting 18% on a reducing-balance basis at best (NB: you never get to fully deduct the costs, and it takes more than 20 years to recover most of the value). You can share only one AIA per group of companies. There is no limit on RDAs, so for companies spending more than £200k, RDAs can potentially sweep up the balance to maximise the deduction.

Any company making or considering a claim for R&D tax relief and incurring capital expenditure should consider RDAs. They can’t always help, but if you don’t bother and miss the deadline for claiming (2 years after the end of the accounting period), you have missed your chance permanently.